-

BackWhat we doNumis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.Investment Banking

-

BackLatest newsRead the latest news about our business, our people and our work, find out about our next events and conferences.News

-

BackWho we areOur collaborative environment and distinctive way of excelling , is nothing without our great people.

-

BackOur board

Numis at a glance

Our Articles

28

Mar 2024

31

Jan 2024

Latest Transactions

London Stock Exchange Group PLC

£1.4bn

Co-global coordinator on the £1.4 billion sell-down of the London Stock Exchange Group PLC

March 2024

Custodian Property Income REIT

£237m

Sole financial adviser, sponsor and corporate broker

January 2024

Numis On Twitter

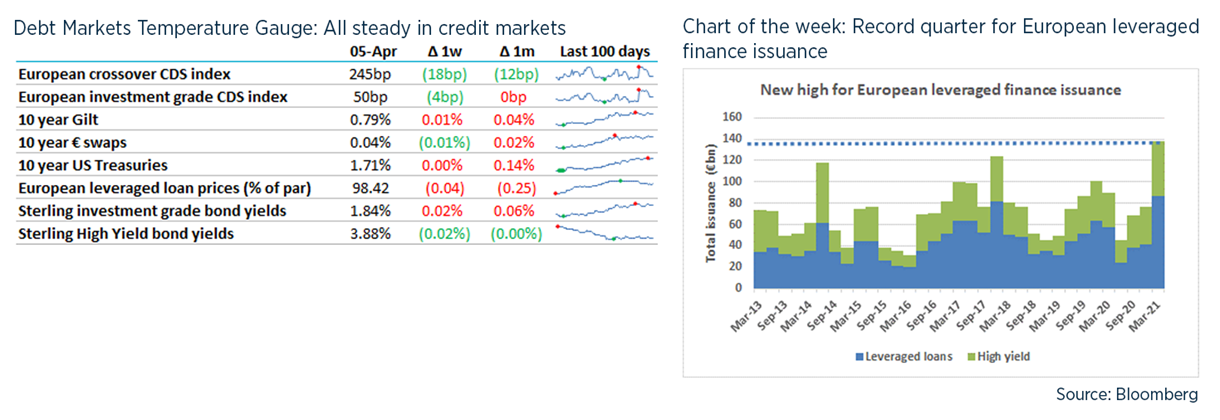

Debt Advisory Update

It was my father’s 80th birthday yesterday and, as we couldn’t have a proper party, we were talking on Zoom about how the world has changed in his lifetime.

He spent his career in computing and appropriately 1941 saw the invention of the Z3, the first ‘real’ computer. This was invented in Germany but dismissed by the Nazis as not “war-important”, and then unfortunately destroyed in a Berlin air raid in 1943. Not every good idea is recognised straight away, as Clive Sinclair found out in 1985 with his forerunner to the now-ubiquitous electric scooters.

I also listened to Epsilon Theory’s podcast about leverage in Archegos, Gamestop / Melvin Capital and Greensill – highly recommended.

TL / DR: End of CCFF and CBILS; Financing Football; Neither Debt nor Equity

1. The end of Covid Financing Acronyms (and a new one)

- March saw the end of CLBILS, CBILS, Bounce Back Loans and new drawings under CCFF. Our clients made the most of these schemes but often the UK government financing support was a bit of a Heath Robinson / Rube Goldberg machine (just a reason to link to my favourite ever music video)

- So what did we (taxpayers) get for our money?

- CCFF lending peaked at £20bn in May 2020 and now provides funding of £7bn to a strange mixture of borrowers: (a) overseas subsidiaries of large multi-nationals like Baker Hughes (b) housing associations and (c) severely Covid-impacted travel and leisure businesses.

- £23bn provided to SMEs under the CBILS (smaller business) 80% guaranteed loans, with average size £236k. But only 42% of these applications were successful.

- The larger CLBILS scheme saw £5.3bn of loans with average size £7m and 63% success rate.

- The highest “success rate” was for the Bounce Back Loan Scheme (100% guaranteed) lent an astonishing £47bn: 74% of applications were approved. Almost half of this was ‘lent’ in the first month to 7 June 2020, with a long tail afterwards.

- It seems 100% guarantees make banks less discriminating. And there may be more reports of fraud once Bounce Back repayment obligations start next month.

- The new Recovery Loan Scheme (“RLS”?) has launched this morning: broadly, it’s similar to the CBILS scheme with loans capped at “£10m per business (max £30m per group)” which I think is aimed at ensuring that no-one abuses this scheme like Greensill exploited the CLBILS to lend £400m to GFG-related businesses.

2. Financing football

- Three football finance stories this week, all connected with Liverpool FC.

- MetLife has lent £117.5m to the English Football League, which had been looking at borrowing from the Bank of England. The EFL Chairman is Rick Parry, ex-CEO of Liverpool, who wants to ensure the clubs can pay wages through this season. The loan is secured on “Solidarity Payments” from the Premier League and it seems that the EFL had been seeking £150-225m, so I hope this is enough.

- Also yet to pay back Bank of England money: the FA (£175m), Arsenal (£120m) and Spurs (£175m).

- Wembley’s lenders are currently being asked to provide more debt for longer.

- NB the pioneer of football finance in the UK was Stephen Schechter, ex Schroders, Lazards and Bear Sterns. Schechter helped Man City, Leeds, Ipswich, Leicester all take on lots of debt in the early 2000s, most of which went pretty badly, as did this tax case.

- Courtesy of Euromoney, and not content with messing around with Greensill and Bill Hwang, Credit Suisse provided debt financing (p3) for Barcelona’s £109m deal for Coutinho. Credit Suisse has arranged full reinsurance of the credit risk from a syndicate of re-insurers, which they hope will go better than it did with Greensill.

- LeBron James invested $750m in Liverpool’s parent company (for unknown % and for unknown votes) after Fenway failed to get a deal away with a SPAC. Let’s hope he knows Bill Shankly’s comment that football is more important than life and death.

3. Not debt but not equity

- As one of my colleagues and I discussed last week, what actually is ‘equity’? It sounds simple: an equal share in the business.

- But it gets complicated: majority voting mean that minority interests can be like leverage: you get to use someone else’s capital while giving them limited voting rights, particularly when combined with super-voting shares. Introducing preferred equity muddies the waters further.

- Cineworld’s new convertible pre-funded the first year of interest (p10 here) as did Gatwick’s recent high yield bond. So while these may be “fixed interest”, some of this is just paid by the initial capital

- My colleagues and I were discussing a proposed investment which involved: non-cash (PIK) interest, no covenants and long-dated maturity. How far away does a repayment obligation have to be before it is no longer concern: forever? 10 years? How about 7 years? At some point, IBGYBG and this reminds me of Keynes’s observation that “in the long run we are all dead”.

- This ‘grey’ area involves negotiating with shareholders, lenders, accountants and possibly rating agencies – everyone has a different take on this dividing line.

UK Financings this week

- Fuller’s has amended and extended its debt facilities out to Feb-23 alongside a successful equity placing that raised £53.6m.

- Two airport deals: Heathrow returning for the second time this month with €500m 9.5 year bond and Gatwick entering the HY market for the first time with a £450m 5NC2 at 4.375% (upsized by £50m).

- Sofina Foods is backing their acquisition of Eight Fifty Group wholly underwritten by Rabobank.

- Anchor Hanover completed a £300m sustainability linked RCF with four banks (Barclays, MUFG, NAB and Santander) – a first for the housing association sector.

- A few more SONIA loans announced this week as well – GCP Infrastructure Investments has agreed a £165m RCF NatWest, Lloyds & AIB and Guiness Partnership a £150m RCF with Lloyds.

- More details on National Grid’s £9.335bn bridging loan with Barclays and Goldman Sachs, with margins ranging from 55bp to 110bp depending on National Grid’s credit rating.

Our services

Numis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.