-

BackWhat we doNumis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.Investment Banking

-

BackLatest newsRead the latest news about our business, our people and our work, find out about our next events and conferences.News

-

BackWho we areOur collaborative environment and distinctive way of excelling , is nothing without our great people.

-

BackOur board

Numis at a glance

Our Articles

28

Mar 2024

31

Jan 2024

Latest Transactions

London Stock Exchange Group PLC

£1.4bn

Co-global coordinator on the £1.4 billion sell-down of the London Stock Exchange Group PLC

March 2024

Custodian Property Income REIT

£237m

Sole financial adviser, sponsor and corporate broker

January 2024

Numis On Twitter

Debt Advisory Update

I’m hoping at least someone has noticed the slight delay to this ‘weekly’: in a busy week, I’ve made Voltaire’s mistake of letting the best be the enemy of the good (or at least, ‘something acceptable’), otherwise known as forgetting the 80:20 rule.

This week: be glad you’re not the pilot of the Ever Given ship, currently impossibly stuck in the Suez Canal like Douglas Adams’ sofa.

TL / DR: IAG’s Lift Off; Prospective Receivables Deals; Fish Ratings

1. IAG’s Lift Off

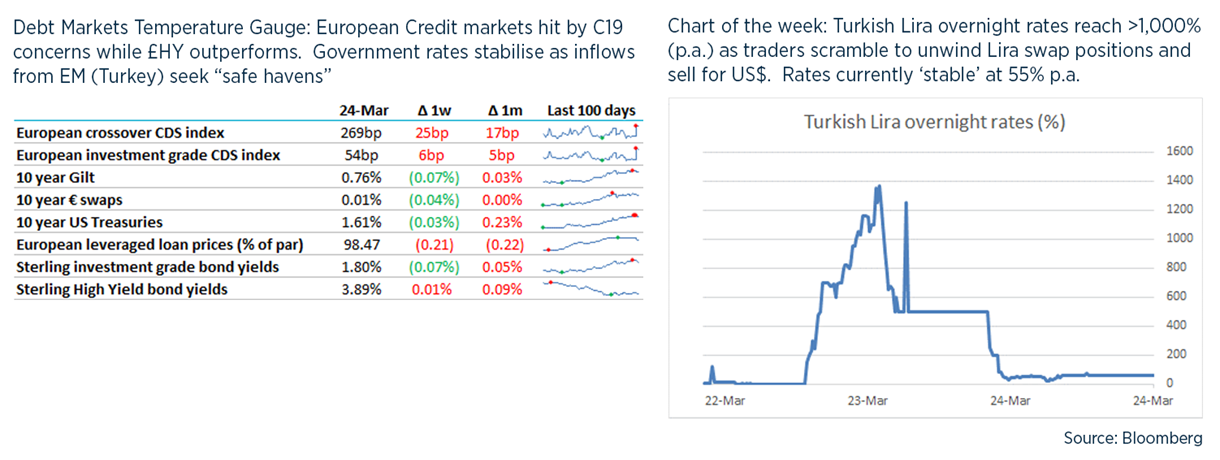

- Priced just before a new wave of pessimism on European C19 and travel, IAG last week raised €1.2bn of 4- and 8-year high yield bonds at a blended rate of 3.3% and spread of 390bp and then followed up this morning with a $1.8bn 3-year secured syndicated RCF. Some highlights:

- Timing / luck: sentiment changes fast – following this week’s volatility, the 2029 bonds are quoted 2pts lower, from being oversubscribed at launch.

- Weak bond covenants: the new HY has no financial covenants and only a weak negative pledge, which permitted the new secured RCF, which wasn’t disclosed to HY investors in advance.

- Slots: IAG has provided security over its slots at Heathrow to RCF lenders. Virgin Atlantic pioneered this in 2016 after BA failed to get a deal away in 2012. Lenders’ rights to realise value from UK slots were strengthened by the Supreme Court decision for Monarch Airlines in 2018.

- IAG / American Express deal: I’d missed this last summer: Amex ‘prepaid’ IAG by £750m to buy Avios points in advance – effectively lending £0.75bn to IAG, to be repaid through flights.

- Potential airmiles securitisation: I’m still getting my head around these. Delta Airlines did one last year which is described here: economically, passengers and partners like Amex are lending to Delta: passengers (particularly their employers) are paying a premium to accrue airmiles, and Amex is paying Delta hard cash, in return for its agreement to fly them in the future – the future cost of which is an operating cost for the airline and senior to all its debt service.

- Asset sales: BA last year sold its art collection for £2.2m including a Bridgit Riley and a Damien Hirst, and its splendid HQ is also up for grabs.

- I’ve just remembered that Arthur Andersen used to have a decent art collection – seems that it was sold by Deloitte in 2008 for £850,000. Anyone who worked at Surrey St may remember this lovely Bridget Riley and this Patrick Caulfield.

Greensill (again)

- I did try to stay away from Greensill this week but it’s like irresistible, like picking a scab.

- This week’s detail came from a US lawsuit filed by Bluestone Resources against Greensill in the US. I recommend reading at least the first part of the filing here, as it describes really well how it takes both a willing lender and a willing borrower to create a truly awful loan. Also note that Bluestone is owned by the family of Jim Justice, the Republican Governor of West Virginia. Perhaps David Cameron could have a word?

- Greensill’s innovative Receivables Purchase Agreement (just 17 pages!) enabled loans against “prospective receivables”: receivables that did not yet exist from buyers that were not yet customers and which had probably never heard of Bluestone! This was part of total financing to Bluestone of $850m, which generated $108m of fees and $100m of equity for Greensill.

- These ‘prospective receivables’ had a short-dated ‘maturity date’ at which point they are ‘rolled’ cashlessly by the replacement of new ‘prospective receivables’. This was accurately described by Bloomberg’s Matt Levine as “payday loans for a job that Bluestone hadn’t even applied for”.

- At its heart then, this was short-term and unsecured leveraged finance. Not a problem if this is your own money, but Greensill was portraying this to its funders (mainly investors in Credit Suisse’s fund and depositors in Greensill Bank) as being short-term and low risk working capital finance. Only after it became obvious that the loans couldn’t be paid back, Greensill started to get proper security and take equity stakes.

- Greensill’s US team was led by Roland Hartley-Urquhart, who 23 years ago filed a patent for the apparent invention of supply chain finance. He also tried to get Bluestone to trade with Gupta’s Liberty Steel despite also saying “if he were in Bluestone’s shoes, he would not ship to GFG”. Hartley-Urquhart also tried to force Bluestone to hire either Rothschild or Morgan Stanley as restructuring adviser, for reasons that are not clear.

Fish Ratings

- On a lighter note, Nicola Sturgeon’s troubles with Alex Salmon provides a reason to link to my favourite ratings agency – Fish Ratings.

- Created by what I hope is a bored credit Fitch ratings analyst, this has been going for a couple of years providing cod ratings reports on global fish stories including a 2021 Global Fish Outlook, Baby Shark (rated as “D” with the rationale “Baby Shark, D, D, D, D, D, D …”), Anchovies on Pizza structured credit rating, and a pair trade on Sturgeon vs Salmon.

- For once, I can’t find any takeaways from this other than its attention to detail is off the scale and could spawn a wave of competitors such as Moonfish’s and Scabbard & Porgy (sorry …)

UK debt financings this week-ish:

- accesso replaced its RCF with a new CLBILS loan from Investec (Numis advised).

- Chrysalis Investments signed a debut £32m RCF with Barclays (Numis advised).

- Everyman Cinemas increased its RCF by £10m to £40m.

- Pendragon extended its £175m RCF by 1 year to March 2023 at a cost of L+485bp.

- Belron raised c. €1bn of leveraged loans at L+250bp to pay a €1.45bn dividend to its shareholders CD&R and D’Ieteren Group. This was accompanied by a credit ratings upgrade by S&P to BB+.

- IAG closed a benchmark €1.3bn high yield financing, split between €500m 4-year notes at 2.75% and €700m 8-year notes at 3.75%. It was oversubscribed with books reaching €5.25bn and pricing tightening 50bp across both tranches. IAG also announced a $1.755bn 3-year RCF secured against aircraft and its landing slots at Heathrow and Gatwick.

- Blackstone Credit provided a £520m unitranche with a £350m acquisition facility to help BC Partners acquire Davies Group alongside an £80m bridge RCF to be taken out by banks.

- Sanne upsized their £150m RCF due Feb-23 into a new £210m facility till Mar-23 (+1+1 extensions) with a syndicate of six banks.

- National Grid is backing their acquisition of Western Power Distribution with a £8.25bn bridge loan from M&A advisers Barclays and Goldman Sachs.

- Youngs has extended its £20m bilateral loan with NatWest out to Nov-21, alongside a £50m 5-year term with NatWest and HSBC.

- SSP has extended the maturity of its £523m (£373m term loans/£150 RCF) loans to Jan-24, by 2 years, alongside covenant amendments and further waivers.

Our services

Numis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.