-

BackWhat we doNumis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.Investment Banking

-

BackLatest newsRead the latest news about our business, our people and our work, find out about our next events and conferences.News

-

BackWho we areOur collaborative environment and distinctive way of excelling , is nothing without our great people.

-

BackOur board

Numis at a glance

Our Articles

28

Mar 2024

31

Jan 2024

Latest Transactions

London Stock Exchange Group PLC

£1.4bn

Co-global coordinator on the £1.4 billion sell-down of the London Stock Exchange Group PLC

March 2024

Custodian Property Income REIT

£237m

Sole financial adviser, sponsor and corporate broker

January 2024

Numis On Twitter

Debt Advisory Update

Happy Chinese New Year and a Merry Six Nations!

TL / DR: rates get interesting; derivatives get dangerous; and how the US got New Orleans

1. Rocketing Rate Rises

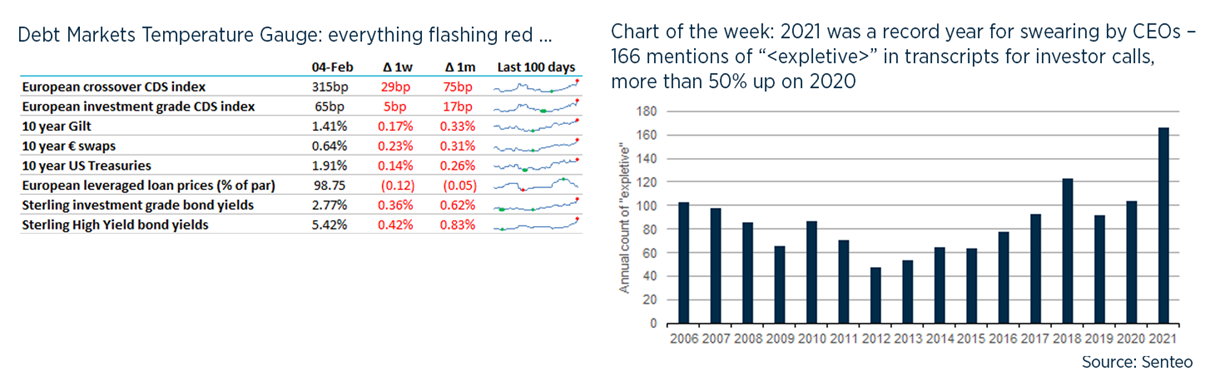

- The Bank of England raised rates by 0.25% to all of 0.50% but the bigger news was that just under half Monetary Policy Committee thought rates should have been raised to 0.75%. The markets immediately priced in rises above 1% by May 2022 - the last time the Base Rate was at this level was January 2009, when Beyoncé was in the charts with Single Ladies (Put A Ring On It).

- Meanwhile over the ECB, I’m not sure Christine Lagarde is really allowed to actually raise interest rates but instead has to make do with talking tough: she is no longer ruling out a rise this year, and markets are expecting the ECB rate to be 0% by the end of the year.

- Longer-dated bond markets have already anticipated this with 10-year Gilts now almost at the same level as they were in 2012 and the German government once again has to pay to borrow money for 10 years, albeit only at 0.2%.

- Real rates remain very negative with 10-year expected inflation (as measured by Gilts) at 4.1%, last seen when John Major and Ken Clarke were partying in Downing Street.

- While rising rates make borrowing more expensive, they will also improve bank profitability – which may encourage lending. This is supported by the Bank of England’s latest survey of credit officers, which indicates they expect to continue to increase loan tenors.

- When discussing future direction of interest rates, I’m always minded to paraphrase Michael O’Leary on fuel hedging: if I knew where rates were going then I’d be a very successful trader instead of running a business. When in doubt, hedge half your risk.

2. Derivative dangers

- With this backdrop, many of our clients have been hedging interest rates, particularly US$. It may be too late to catch the bottom of the market but <2% for 10 years still looks pretty good by historical standards: 10-year rates have averaged 4.75% since 1989.

- Executing this hedging can require expensive and complicated documentation, as derivatives have credit exposure: ask anyone who has ever won a bet but when the loser has refused to pay.

- Markets can move against either counterparty in a transaction and they may not want or be able to pay when the bill comes. For example, in 2005 you might have agreed to pay 3% for 5 years in return for receiving Libor (this was the market rate); this felt pretty stupid when Libor then averaged 0.7% over the next 5 years. And if you failed to pay then the swap counterparty would become an annoyed creditor.

- This potential credit risk exists as soon as you enter into the transaction, where the loss is a bit like Schrodinger’s Cat. You might only be concerned about the scenarios where your counterparty defaults when they owe you money, but your counterparty is concerned about the opposite scenarios. Banks measure this as “potential future exposure” or PFE, and they may require collateral (or indeed, you may ask the banks to post collateral).

- In 80 Days Around the World, Phileas Fogg foresaw that he might not be able to honour his bet (because he could be dead) and, being a man of utmost honour, he left his cash with the Club steward. Similarly derivative counterparties can also require collateral – sometimes triggered by any deterioration in credit standing – as Centrica found to its cost a few years ago and which may have prompted its sale of its energy supply division.

- I see the energy crisis in the UK through this lens: consumers entered into long-term agreements at low rates with smaller suppliers naturally expecting these suppliers to honour the deal. But some of these suppliers did not hedge themselves enough by entering into long-term supply agreements with electricity producers – maybe because they expected prices to fall or because the producers required more collateral than the suppliers were able to provide.

- After all, ‘high’ prices can fall leaving thinly-capitalised suppliers on the hook to pay ‘excessive prices’ and so suppliers want to know their long-term contracts will be honoured.

- And so some of these suppliers went bust as they had more going out than coming in. In the words of the AIG Vice Chairman “the left side of the balance sheet has nothing right and the right side has nothing left”. In related news, the French government has required EdF to take a loss equivalent to 20% of its market cap to hold energy bills steady – a form of expropriation.

- Elsewhere in derivatives, Bloomberg reported that Barclays took a loss of $100m on a “deal contingent” hedge for Advent. This is effectively a FX deal which falls away if the acquisition fails. I suspect Barclays lost less than this, as it is likely to have only partially hedged its position and / or used options.

- Like many strategies which involve selling optionality, this sort of business can look like picking up pennies in front of steamrollers – it can look great as it is short-dated with limited credit or funding costs. More positively, pricing is skewed in banks’ favour as many PE bidders need these hedging trades given they would struggle to fund an aborted hedge.

- But fundamentally these trades require banks to bet on whether M&A deals are going ahead, which is not something that can easily be managed or hedged.

- Most banking is intermediating and / or transforming risks between investors – taking directional bets is for a hedge fund. Maybe the banks should repackage this M&A risk into a product for merger arbs?

{kind=link}

3. Financing the Louisiana Purchase

- Not really topical, but I came across an amazing piece on how Barings financed the US purchase of Louisiana from Napoleon in 1803 for $15m (about $342m in today’s money).

- At the time, US GDP was about $514m and UK GDP was about $2bn. So for about 3% of its GDP, the US doubled its land area – 830,000 square miles at about $0.03 / acre.

- The French were short of cash after losing in Haiti and were ready to retreat from the Americas. After initially discussing selling just New Orleans and Florida for $10m, the French decided that the rest of Louisiana was pointless on its own (sorry Biloxi!) and invited offers for the whole thing.

- Barings teamed up with a Dutch bank called Hopes and haggled the French down from FF100 million to FF80m, which was $15m at the agreed exchange rate of $1 = FF5 ⅓ (no deal contingent hedging carried out so far as we know). Apparently technically Barings bought Louisiana and then back-to-back resold it to the US.

- US government assumed FF20m owed by French citizens to US citizens and issued $11.25m of bonds to France at 6% (for reference Inter Milan recently agreed to pay 6.75% on its bonds). The bonds were repayable in equal annual instalments after 15 years. The bonds were transported to Europe in triplicate on separate boats in case one sank.

- However, the French wanted their money sooner – and were not afraid of financial engineering (something which continues to this day). So Barings then bought the bonds from the French for $9.7m in cash i.e. at a 13.5% discount to face value. Barings also staged its payments to the French over 2 years (they actually later accelerated this for a 3% further discount).

- Barings then marketed these bonds to investors in London, Netherlands and the US at or above face value – this was completed within a year. It helped that they more or less controlled the markets.

- It’s got elements of Trading Places, Greensill and Pirates of the Caribbean. Who said finance was dull?

- Overall, I estimate Barings made a net profit of $2.7m over the 12 months, an IRR of over 30% and a Money Multiple of about 1.2x. But as with any private equity investment, you need to reinvest this quickly: Barings built US railroads, which also turned out well.

Recent UK Financings so far in 2022

Loans

- Supermarket Income extended its RCF by £137m to £250m for 2 years at SONIA +150bp.

- Caffe Nero received £330m of debt from Carlyle which enabled the recapitalisation and buyout of the EG Group / Issa family.

- Micro Focus arranged $1.6bn of 5-year term loans in EUR and USD, alongside a new $250m 5-year RCF. Numis advised Micro Focus.

- ITV agreed a new £500m RCF, downsized from its previous £630m revolver, with pricing linked to its Scope 1-3 emissions. Barclays, BNPP, Mizuho, NatWest and Wells Fargo are lending.

- Burberry signed a new £300m sustainability-linked RCF, linked to its Scope 1-3 carbon emissions.

- Workspace agreed a new £200m sustainability-linked loan for 3-years ag L+165bp.

- EMIS increased its RCF to £60m from £30m.

- Restore refinanced on an unsecured basis and upsized to £200m for 3+1+1 years.

- Harworth agreed a £200m 5-year RCF with NatWest, Santander and HSBC.

- Photo-Me (yes I thought they had disappeared too) has arranged £202m of loans with Credit Agricole to support its take-private by its CEO. Unusually, this is a 6+6m term, which must mean there is some other financing going on in the background.

- IOMart signed a £100m RCF at SONIA +180bp for 3.5 years.

- Dunelm signed a £185m RCF for 4+1+1 years where the margin will moved +/- 2.5bp linked to 4 sustainability targets.

- Hill Group signed a £220m 5-year RCF with pricing linked to 4 sustainability targets, with Lloyds, Natwest, HSBC and Santander.

- Rentokil signed a $2.7bn bridge for a US acquisition, provided by Barclays.

- M&S signed a £850m 3.5 year RCF with pricing linked to delivery of its Net Zero target by 2040. This is £250m smaller and only 2 years longer than its previous RCF.

- Vistry closed a new RCF with pricing linked to carbon emissions, delivering affordable housing and training apprentices.

- Severfield signed a 5-year £50m RCF from HSBC and Yorkshire Bank.

- Smith News extended its loan facilities by 18 months by raising margins to SONIA+425bp and capping dividends until it has deleveraged.

- Ernst & Young signed an RCF with pricing linked to EY’s air travel emissions, volunteering, and increasing diversity in its partner ranks.

- Jaguar Land Rover signed a £625m 5-year loan which was 80% guaranteed by the UK’s Export Credit Agency – this time for R&D and export of EVs.

PPs

- Not UK, but Real Madrid FC raised €225m in the USPP market at 1.53%.

Bonds: January was a record month

- Wizz Air priced its first EUR deal, of €500m for 4-years at ms+105bp, which was 40bp inside indications.

- Motability sold a £500m 20-year social bond at G+90bp, for a coupon of 2.125%.

- Sage Group (BBB+) priced its second public bond, £400m for 12 years at 2.875% (G+150bp).

- Thames Water (Baa1 / BBB+) priced a €1.15bn Green EUR bond across 6 and 10 years at ms+75bp and ms+100bp.

- Flagship Group (A2) sold £50m of sustainable bonds at 2.38%.

- Futures Treasury (A+) tapped its 2044 bond at G+95bp.

- Housing 21 issued £80m 27-year bond at G+120bp.

- London & Quadrant printed £300m 10-year sustainability linked bond at G+87bp.

- National Grid priced €1bn of 4- and 9-year bonds at ms+44bp and ms+77bp.

- BP printed $2bn of 10-year bonds at T+95bp.

- Zenith Finance (car rental) (B1 / B+) priced £475m of 5.5 year HY bonds at 6.5%.

- Voyage Care (B2 / B+) priced £215m of 5-year HY bonds at 5.875%.

- True Potential priced £400m sterling HY alongside €360m HY at 6.5% and 5% respectively (both 5-year).

Our services

Numis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.