-

BackWhat we doNumis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.Investment Banking

-

BackLatest newsRead the latest news about our business, our people and our work, find out about our next events and conferences.News

-

BackWho we areOur collaborative environment and distinctive way of excelling , is nothing without our great people.

-

BackOur board

Numis at a glance

Our Articles

28

Mar 2024

31

Jan 2024

Latest Transactions

London Stock Exchange Group PLC

£1.4bn

Co-global coordinator on the £1.4 billion sell-down of the London Stock Exchange Group PLC

March 2024

Custodian Property Income REIT

£237m

Sole financial adviser, sponsor and corporate broker

January 2024

Numis On Twitter

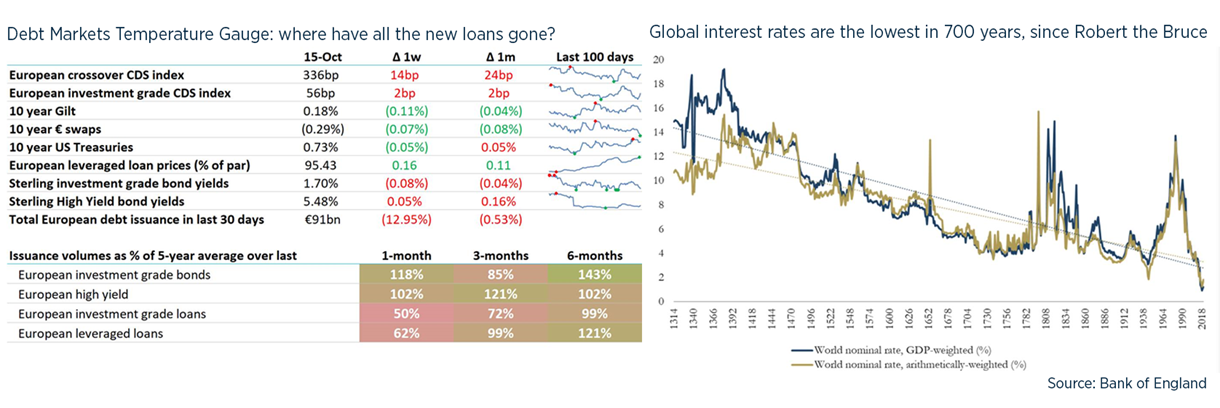

Debt Advisory Update

Your weekly lines on liabilities.

TL/DR: Bank of England as a futurologist; Return of the MAC; Revolving RCF lenders

1. The Bank says that likes to say … “no”

- The Bank of England quarterly survey of Credit Officers is always worth persevering with, despite the format and prose style.

- I know a few of the credit officers being surveyed, and they do take it seriously: it genuinely provides a window in the soul of the UK loan credit officers and just how miserable they are currently feeling – more to the point, these are the actual people who are approving lending so how they are feeling affects us all.

- Latest views: worth digging through Annex 3 here, to find out what credit officers expect over the next 3 months:

- A worse appetite for credit risk from their bank(s).

- Lower demand and lower provision of total credit lines – but this is driven primarily by reduction in capex funding and reduction in real estate loans, with acquisition financing expected to be more in demand.

- Higher demand for acquisition financing from borrowers.

- Pair this survey with Deloitte’s CFO survey which shows that 40% of CFOs think UK corporate balance sheets are overleveraged (p4 here).

2. Return of the MAC?

- Material Adverse Change clauses (“MAC” or Material Adverse Effect “MAE”) are pervasive in corporate loans – usually an event of default if something happens that is “materially adverse” to (i) the business, [assets, financial condition, operations] or (ii) its ability to comply with payment obligations under the loan [maybe plus certain other loan obligations]. Other bells and whistles can be applied.

- The thing is, I’ve never seen this Event of Default actually used by the banks to effect a default or drawstop. The law firms got very exercised about this March (e.g. Shearman here) but so far it is the dog that didn’t bark.

- There is now a leading English legal case that may well shed some light on whether this might be available: more here courtesy of Mayer Brown.

- Wex agreed in January to buy two travel sector payments companies (eNett and Optal) from Travelport for $1.7bn; Wex then claimed in May that there had been a MAC caused by COVID. The SPA is under English law so its final judgement will be relevant to most UK borrowers.

- It’s quite a convoluted MAC definition but the first hurdle for Wex has been cleared by the Court (judgement here) which opens the way for assessment of whether COVID constitutes a MAE for these businesses as compared to other B2B payments operators – which seems likely to me.

3. Revolving RCF providers

- It’s typical in corporate loans to enable lenders to transfer their commitments to other banks “with borrowers’ consent, not to be unreasonably withheld”.

- Other versions are possible, such as a “whitelist” (used in European leverage finance) or “blacklist” (US leveraged finance). All bets are off if there is a default.

- Mostly the banks view their RCF commitments as a “ticket to play” in ancillary business and so want to hang on to them – unless the borrower enters distress e.g. Barclays and Lloyds selling their Interserve loans to Emerald as described here.

- But sometimes lenders will sell out if their management decides the “ticket price” of the loan is too expensive for the ancillary business on offer – it’s never favoured by relationship manager but often happens when the bank is going through a purge of unprofitable relationships. For undrawn RCFs, this usually involves the outgoing lender paying a fee to the incoming lender equivalent to selling out at 85-95p / £.

- We are hearing of increased disposals by one leading UK High St bank, which is consistent with what we are seeing of their responses to new lending opportunities.

- Overall, this reinforces our view that corporate loan markets are going to be much tougher over the next year, as banks seek to rebuild profitability.

UK debt financings this week:

- Rolls-Royce books closed books on (twice) upsized deal from £1bn to £2bn(!) equivalent: €750m 2026 tranche at 4.625%, £545m 2027 tranche at 5.75% , $1bn 2027 tranche at 5.75%. All non-call life.

- Just Group: Completed its £250m green tier 2 capital raise via a BBB rated 10.5-year, 7% non-call 5.5-year bond issue.

- Heathrow returns to the bond markets with £1.4bn eq class A bonds – 8-year GBP spread 260bp.

- Serco announced the issuance of $200m of US Private Placement Notes with maturities of 5, 7, 10 and 12 years (weighted average of c.8 years with an average interest rate of 3.6%).

Our services

Numis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.