-

BackWhat we doNumis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.Investment Banking

-

BackLatest newsRead the latest news about our business, our people and our work, find out about our next events and conferences.News

-

BackWho we areOur collaborative environment and distinctive way of excelling , is nothing without our great people.

-

BackOur board

Numis at a glance

Our Articles

28

Mar 2024

31

Jan 2024

Latest Transactions

London Stock Exchange Group PLC

£1.4bn

Co-global coordinator on the £1.4 billion sell-down of the London Stock Exchange Group PLC

March 2024

Custodian Property Income REIT

£237m

Sole financial adviser, sponsor and corporate broker

January 2024

Numis On Twitter

Debt Advisory Update

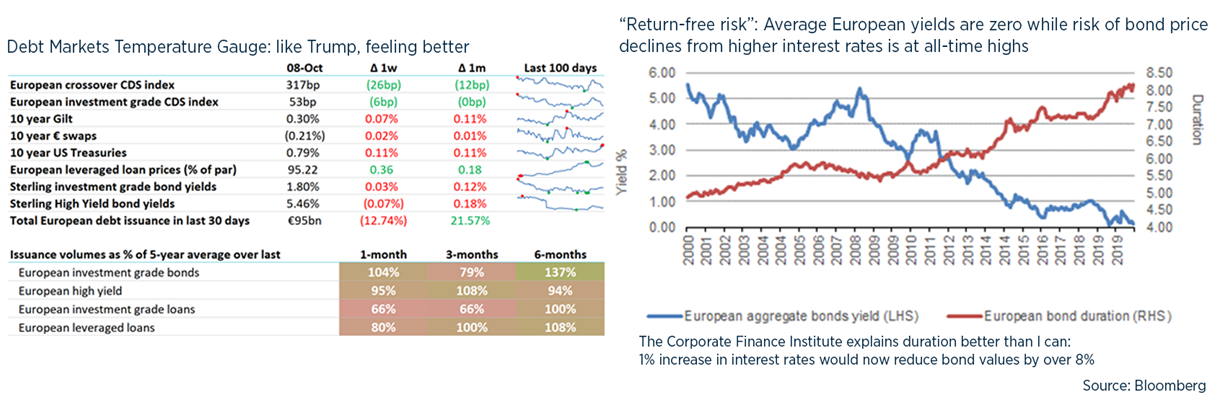

I put last week’s Weekly on LinkedIn and it got over 6,000 views – I’m feeling the pressure like newly-successful bands who are then faced with the difficult second album.

TL/DR: Exhibitionism; High yielding high yield; Lots of leverage

Exhibitionist goes public

- Private placement bonds have long been a stepping stone for growing businesses between cosy bank syndicates and public bond markets. Terms can be tailored for each circumstance – with the exception of financial covenants which remain a pre-requisite

- Just as COVID saw many borrowers reach out to their banks for covenant relaxation, so did PRICOA, Met Life and the Modern Woodmen of America also have had to reach agreement on covenant changes

- But several borrowers, including notably Informa last week, have now replaced US private placements with public debt – with no financial covenants. It’s not cheap: I estimate a make-whole premium cost for Informa of c. 16% of notional, and its new bonds also have a coupon-step of 125bp if it gets downgraded below investment grade – now just one notch away

- Informa is also attempting to remove financial covenants – the prepayment at a premium is part of a package to persuade its PP investors to go along with this

- It will be interesting to see if Compass follows suit, given how hard it found to negotiate USPP covenant amendments back in May

“Give me a lever long enough … and I shall move the world” – different sorts of leverage

- We’ve recently been working with a business that is publicly sub-investment grade on account of its leverage, which has consistently been c.3x due to acquisitions

- Yet this business has seen no change in net debt during COVID, despite seeing c. 10-20% fall in revenues and not raising equity or selling assets

- It has low operational gearing because most of its costs are truly variable, being largely non-labour input costs: drop through from revenue to profit is pretty low. ND / EBITDA has risen only by 1x. Moreover, the business has a cov-lite structure

- Compare this to Compass: without its £2bn rights issue, its credit ratings-adjusted leverage would have risen from 1.3x last year to 3.6x in 2020

- its cost base is largely fixed, being people and rent

- And much of its long-term bonds had financial covenants …

- Other forms of non-financial leverage to watch out for: operating leases, ongoing pension deficit repair payments, non-wholly-owned subsidiaries. Even non-voting shares are a form of leverage for the shareholders lucky enough to get to vote

Higher High Yield

- A few interesting deals in the High Yield markets this week showed the various tools available to sell difficult deals

- Rolls-Royce is out for £1bn eq, Jaguar Land Rover is back in US HY markets for $700m, Puma Energy aborted a $300-650m issue, and DNEG (a film visual FX business) is in the US markets for $375m

- Price: this is being tried by them all. RR is whispering yields at 6% area, JLR priced at 7.75%, Puma Energy tried “mid 8%s” before aborting and DNEG came out with 8.25-8.5% and may look at >9%

- Tenor: shorter is easier, e.g. JLR, DNEG and Puma are all out with 5 year tenors, which is the shortest standard length

- Terms: JLR has promised not to subordinate its new unsecured bondholders by giving security to new creditors (called ‘priming”, as used by Carnival this year)

- Guaranteeing returns: high yield bonds are usually capable of being repaid in the final few years without penalty. Rolls-Royce is apparently using a “non-call life” structure to reassure bondholders that they won’t lose out if Rolls ‘gets better’

- Getting the Street onside: JLR used 23 (yes twenty-three!) bookrunners

UK debt financings this week:

- Tesco agreed a £2.5bn three-year syndicated revolving credit facility (RCF) with a margin based on risk free rates (RFRs) - The financing is the first syndicated loan in the UK that uses RFRs for sterling and dollars rather than Libor.

- Chrysaor’s takeover of Premier Oil is being backed with a US$4.5bn seven-year reserve-based lending (RBL) facility. This was underwritten by Bank of Montreal, BNP Paribas, DNB and Lloyds

- Tullow Oil plc announced that a RBL redetermination confirmed debt capacity of $1.8bn and headroom of $500m, which is down by $100m from April’s determination.

- ECI is raising debt to refinance the all-equity bridge put in place to acquire Mobysoft from Livingbridge. Feedback is for 3-5x which is a little less than had been anticipated.

- Pizza Express completed another stage in its restructuring – but this will take years to finally finish …

Our services

Numis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.